The Invisible Hands Of The Market: Supply and Demand

- Aditya Chintaluri

- Dec 8, 2024

- 3 min read

1. Demand

Definition: The quantity of a good or service that consumers are willing and able to buy at a particular price.

Factors Affecting Demand:

Price: Inverse relationship with demand

The diagram represents the inverse relationship between demand and price.

As demand increases, producers increase the price to gain more revenue(Pe to P1).

As demand decreases, prices are lowered in order for producers to gain more revenue(Pe to P2).

A point to note is that in this example, supply remains constant and doesn’t change.

The price change is due to the increase in demand, a change in demand due to change in price is called an extension/contraction in demand.

Contraction in demand can be defined as a decrease in demand DUE to an increase in price.

Extension in demand is an increase in demand DUE to a decrease in price.

Income: As income changes, spending is also likely to change , the two types of goods that income is spent on can be classified as:

1.Normal Goods: Demand for goods increases as income increases.(eg: food,clothing)

2.Inferior Goods: Demand for goods decreases as income increases(eg:Toned milk which faces a reduction in demand while full cream milk experiences an increase in demand)

Price of Related Goods:

1.Substitutes: An increase in the price of one good increases demand for its substitute (eg: tea and coffee).

2.Complements: An increase in the price of one good decreases demand for its complement (eg:cars and petrol).

Consumer Preferences: Changes in tastes or trends can shift demand.

Population Changes: More people = greater demand.

Expectations: Expectation of future changes in price can affect the present demand. If consumers expect prices to rise in the long-run, there will be an increase in demand for the products in the short-run.

2. Supply

Definition: The quantity of a good or service that producers are willing and able to sell at a particular price.

Factors Affecting Supply:

Price:Higher price leads to greater supply; conversely, supply decreases when price decreases. The relationship between price and supply is positive.

An increase in supply leads to a surplus which results in a lowered price(S to S1 and Pe to P1).

A decrease in price leads to scarcity and increased prices(S to S2 and Pe to P2)

Expansion in supply is an increase in supply along with price(Pe to P2 and Qe to Q2).

Contraction in supply is a decrease in supply along with price(Pe to P1 and Qe to Q1)

Costs of Production: Increased production costs can lead to a decrease in supply.

Technology: Advances in technology can increase supply as more amount of goods can be produced with the same productive potential

Taxes and Subsidies

1. Taxes: Indirect taxes are imposed on firms/producers by the government to gain government revenue. It can also be imposed to reduce the supply of the good(Demerit goods)

2. Subsidies: Subsidies are granted to help an industry or firm by offering an incentive to continue production and not quit the market.

Price of Related Goods:

1.Substitute goods-Goods that can be used to fulfil the same purpose(Physical books and e-books)

2.Complementary goods-A good which is used along with another good(Automobiles and fuel)

Expectations: Changes in the supply curve are possible based on what producers expect to happen to price in the future

Natural Factors: Weather, natural disasters, etc., can influence supply, especially agricultural

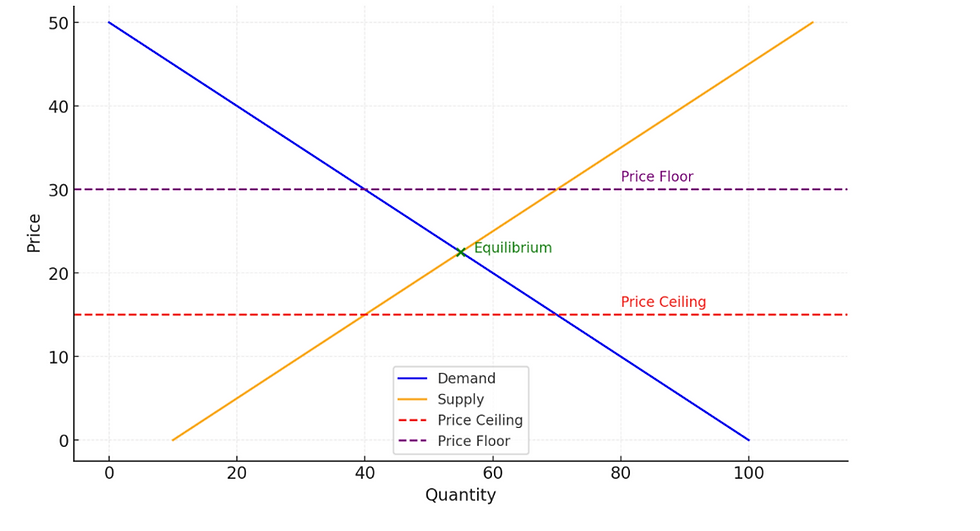

3. Equilibrium

Definition: The point where demand equals supply, determines the market price and quantity.

Disequilibrium:

Excess Demand: When the price is below equilibrium, then there are shortages.

Excess Supply: When the price is above equilibrium, then there are surpluses.

4. Price Elasticity

Price Elasticity of Demand (PED) | Measures responsiveness of quantity demanded to price changes. | PED = (% Change in Quantity Demanded) / (% Change in Price) | - Elastic: PED > 1 (Sensitive to price changes) - Inelastic: PED < 1 (Less sensitive to price changes) | - Availability of substitutes - Necessity or luxury - Proportion of income allocated to the good |

Price Elasticity of Supply (PES) | Measures responsiveness of quantity supplied to price changes. | PES = (% Change in Quantity Supplied) / (% Change in Price) | - Higher PES means greater responsiveness of supply to price changes | - Production capacity - Time period - Stock availability |

5. Applications

Government Intervention:

Price Ceilings: Maximum price below equilibrium (e.g., rent control).Done by the government to make the product more affordable for the public, imposed on items such as food and medicine

Price Floors: Minimum price above equilibrium (e.g., minimum wage). Ensures producers don’t get exploited.

Market Efficiency: Supply and demand efficiently allocate resources.

Comments